Performs double exponential smoothing using the following equations:

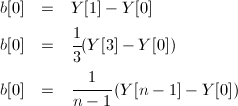

Smoothing scheme begins by setting S[0] to Y[0] and b[0] to pne of the following choices:

Different initialization methods are controlled by the InitMethod parameter. Default value (0) uses first equation, setting it to (1) means the second equation will be used and setting it to (2) means the third equation will be used to initialize b[0].

The first smoothing equation adjusts S[i] directly for the trend of the previous period, b[i-1], by adding it to the last smoothed value, S[i-1]. This helps to eliminate the lag and brings S[i] to the appropriate base of the current value. The second smoothing equation then updates the trend, which is expressed as the difference between the last two values. The equation is similar to the basic form of single smoothing, but here applied to the updating of the trend.